Archives

The security risk continues to weigh heavily

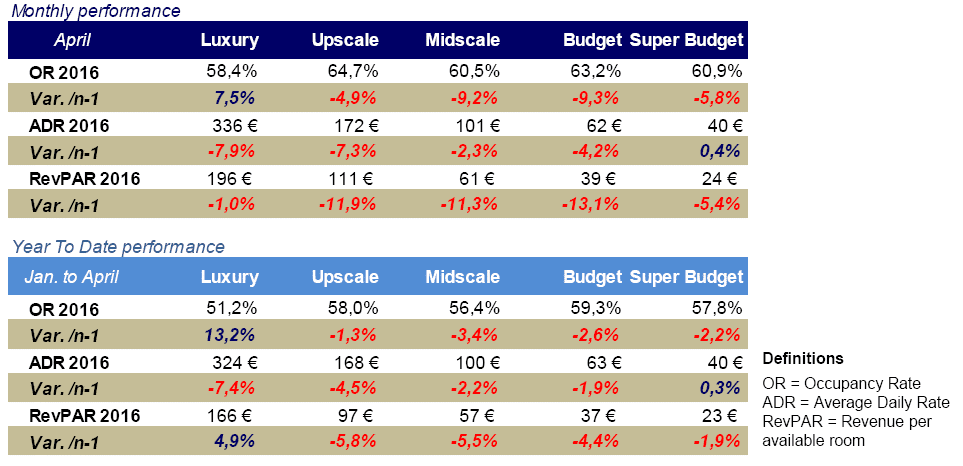

in Brussels at the end of March reminded international visitors of the ongoing security threat in this part of Europe. The school holiday and events calendars were also somewhat unfavourable in April, which accentuated the weak trading activity during this period.

in Brussels at the end of March reminded international visitors of the ongoing security threat in this part of Europe. The school holiday and events calendars were also somewhat unfavourable in April, which accentuated the weak trading activity during this period.The first trimester ends on a positive note

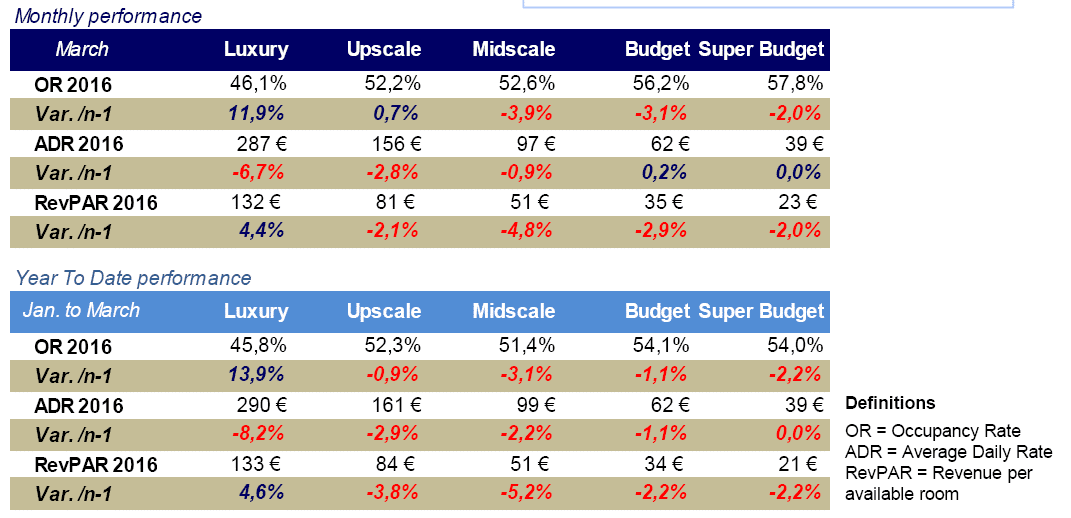

No doubt we will have to wait to see what the real trend is, but March’s results were generally positive. Regional France, and the Côte d’Azur in particular, showed a good start to the year, with the Luxury segment leading the way. Even though Paris and Ile-de-France were still recording lower performances, the declines are lessening. Note that for the first time in a long time, Super-budget hotels saw simultaneous growth in occupancy and average rates.

No doubt we will have to wait to see what the real trend is, but March’s results were generally positive. Regional France, and the Côte d’Azur in particular, showed a good start to the year, with the Luxury segment leading the way. Even though Paris and Ile-de-France were still recording lower performances, the declines are lessening. Note that for the first time in a long time, Super-budget hotels saw simultaneous growth in occupancy and average rates.Paris must wait for recovery

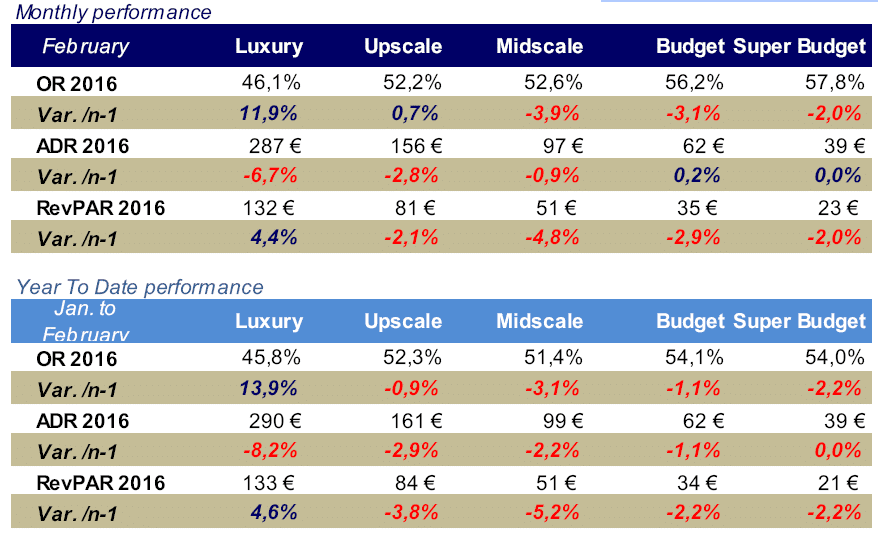

In a similar vein to 2015 and January 2016, the Côte d’Azur and Regional France confirmed or even improved on January’s good results. Conversely, Paris and major Ile-de-France zones continued to record significantly lower performances, and the return to normality will have to wait.

In a similar vein to 2015 and January 2016, the Côte d’Azur and Regional France confirmed or even improved on January’s good results. Conversely, Paris and major Ile-de-France zones continued to record significantly lower performances, and the return to normality will have to wait. 2016 begins as 2015 ends

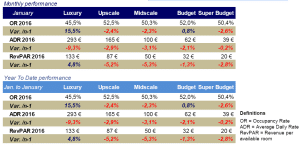

Late 2015 was heavily impacted by November’s tragic events, and Parisian hoteliers were hopeful that January would signal a return to normality. However, they will have to wait, since 2016 began in the same way as November and December 2015 ended.

Late 2015 was heavily impacted by November’s tragic events, and Parisian hoteliers were hopeful that January would signal a return to normality. However, they will have to wait, since 2016 began in the same way as November and December 2015 ended.

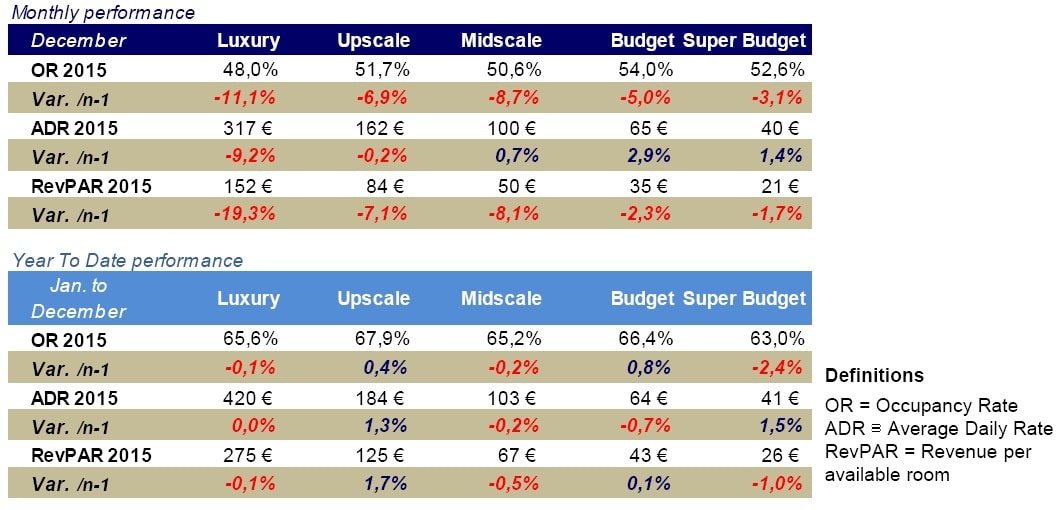

The year ends in the red

A s unfortunately feared, the month of December failed to reverse the trend observed throughout 2015, which ended on a mixed note. Occupancy dropped sharply in all categories in Paris and the Ile-de-France region as a whole, as the impacts of the terrorist attacks were strongly felt. The final month of the year was also challenging elsewhere in France. However, the relative weighting of December compared to the rest of the year meant that the overall good performances achieved up till then in regional France held.

s unfortunately feared, the month of December failed to reverse the trend observed throughout 2015, which ended on a mixed note. Occupancy dropped sharply in all categories in Paris and the Ile-de-France region as a whole, as the impacts of the terrorist attacks were strongly felt. The final month of the year was also challenging elsewhere in France. However, the relative weighting of December compared to the rest of the year meant that the overall good performances achieved up till then in regional France held.

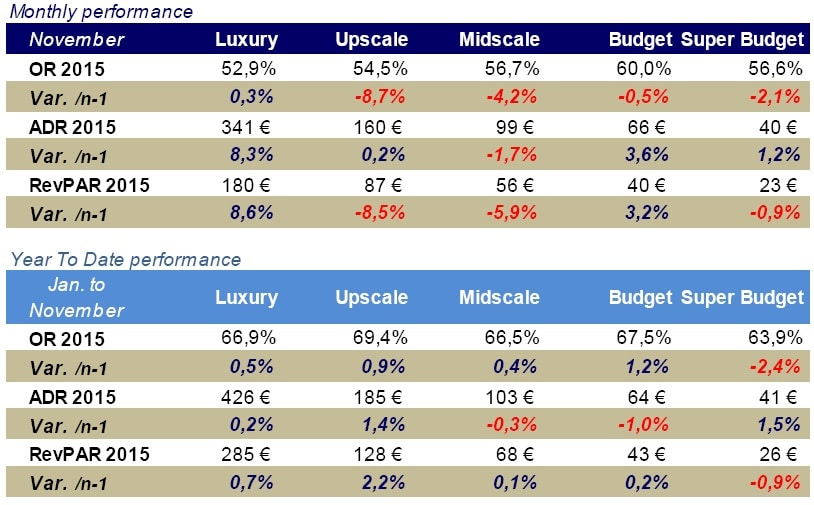

Paris endures

Paris and the Ile de France region were dramat ically hit by two terrorist attacks in 2015. The impact on hotel activity is evidently substantial and hotels in this area will finish the year on a lower note. November saw a fall in occupancy in Parisian hotels of all categories compared to the same period 2014. Although the impact appears to have been less strong in regional France, intermediary categories nonetheless recorded lower performances in November 2015, particularly on the Côte d’Azur.

ically hit by two terrorist attacks in 2015. The impact on hotel activity is evidently substantial and hotels in this area will finish the year on a lower note. November saw a fall in occupancy in Parisian hotels of all categories compared to the same period 2014. Although the impact appears to have been less strong in regional France, intermediary categories nonetheless recorded lower performances in November 2015, particularly on the Côte d’Azur.

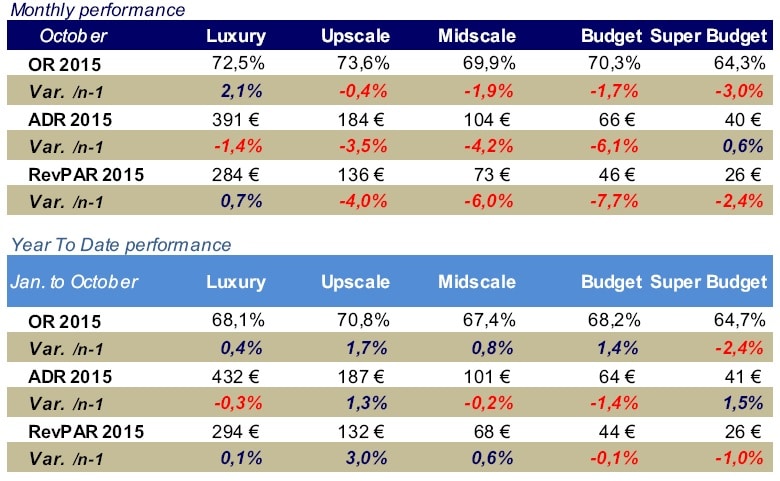

October may mean a difficult end to the year

As the m onths go by, the pattern observed thus far is becoming stronger. Although year-to-date performances at the end of October were more or less balanced, October marked a strong decline in almost all categories, compared (true) to a good October 2014. The sharp drop in Ile-de-France hotel performances was decidedly the most striking feature and dragged down average performance in France as a whole.

onths go by, the pattern observed thus far is becoming stronger. Although year-to-date performances at the end of October were more or less balanced, October marked a strong decline in almost all categories, compared (true) to a good October 2014. The sharp drop in Ile-de-France hotel performances was decidedly the most striking feature and dragged down average performance in France as a whole.

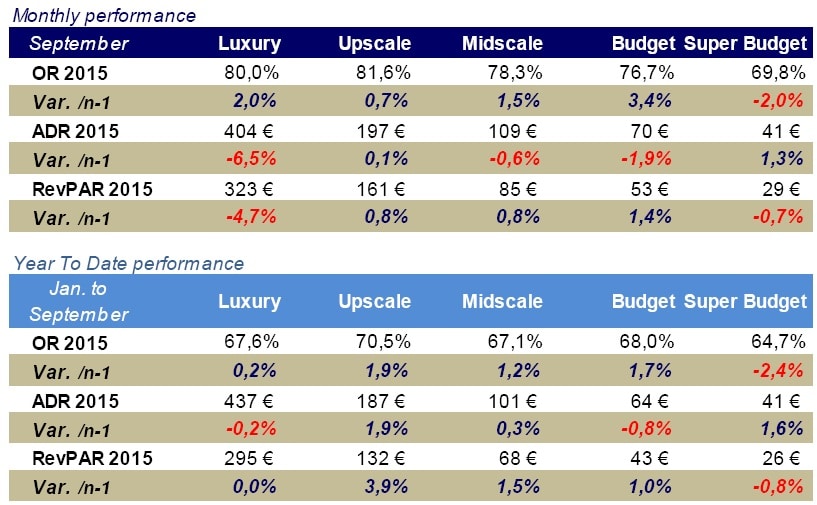

Ile-de-France’s hotels are struggling

Sep tember was encouraging for hotels on the Côte d’Azur and in regional France as they continued to post growth in occupancy and average rates. On the other hand, having stagnated, or even declined, in recent months, Parisian hotels struggled. Although year-to-date performances at the end of September are slightly higher than last year, the final trimester is important in determining 2015’s end result.

tember was encouraging for hotels on the Côte d’Azur and in regional France as they continued to post growth in occupancy and average rates. On the other hand, having stagnated, or even declined, in recent months, Parisian hotels struggled. Although year-to-date performances at the end of September are slightly higher than last year, the final trimester is important in determining 2015’s end result.

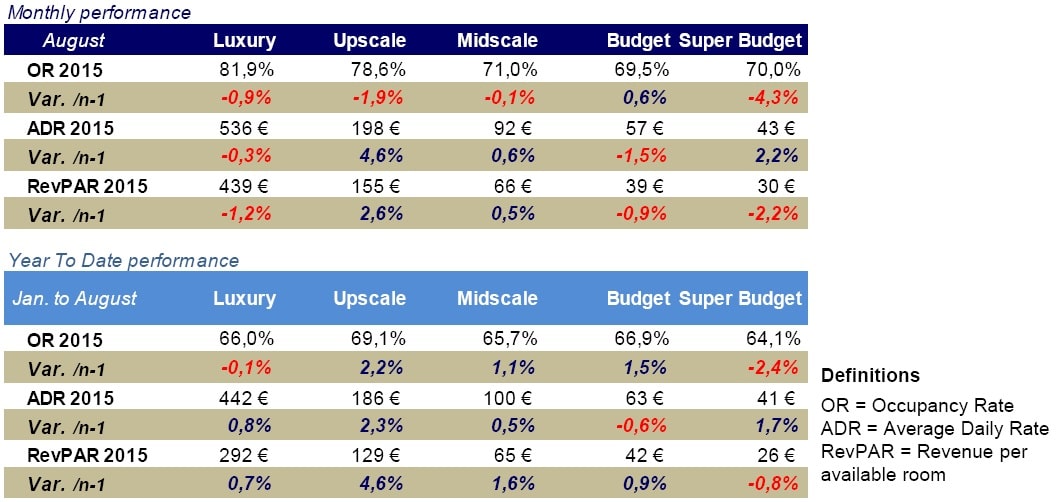

August : An upbeat mood on the coast; more disparate elsewhere

After two months of recovery, August showe d mixed results depending on category and location. While “intermediary” categories (Midscale, Upscale) resisted well thanks to higher average rates, Super-budget hotels confirmed declines in RevPAR. For higher-end hotels, August’s results varied from region to region, resulting in an overall drop in occupancy and rates. Despite all this, August’s results must be put in perspective when compared with August 2014 – a particularly good month – and year-to-date growth, which remains positive.

d mixed results depending on category and location. While “intermediary” categories (Midscale, Upscale) resisted well thanks to higher average rates, Super-budget hotels confirmed declines in RevPAR. For higher-end hotels, August’s results varied from region to region, resulting in an overall drop in occupancy and rates. Despite all this, August’s results must be put in perspective when compared with August 2014 – a particularly good month – and year-to-date growth, which remains positive.

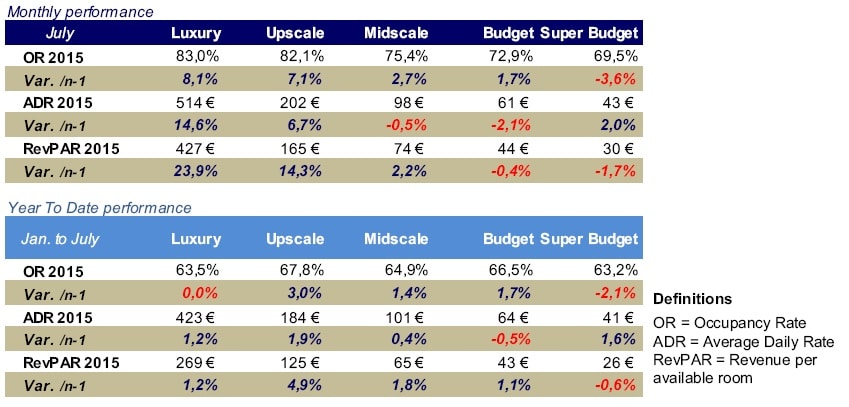

In the July sunshine, the recovery takes hold

Look ing at June’s results, we had dare hope that the French hotel industry was on the road to recovery – July’s performance helped confirm our hopes, particularly at the upper end of the scale. The clement weather in July was obviously one reason for this. However, depending on the region and the hotel category, the shift in Ramadan also had a positive effect. The only fly in the ointment was the Budget and Super-budget categories who failed to benefit from this bright spell.

ing at June’s results, we had dare hope that the French hotel industry was on the road to recovery – July’s performance helped confirm our hopes, particularly at the upper end of the scale. The clement weather in July was obviously one reason for this. However, depending on the region and the hotel category, the shift in Ramadan also had a positive effect. The only fly in the ointment was the Budget and Super-budget categories who failed to benefit from this bright spell.